The Council meeting was followed by a press conference highlighting the key decisions taken during the meeting, including the decriminalization of GST offenses and measures to simplify GST compliance. Let’s examine them in more detail.

Key Highlights

Overview:

On 17 December, the GST Council held its 48th meeting virtually. The meeting was chaired by Smt. Nirmala Sitharaman (Union Finance Minister), and attended by Shri Pankaj Choudhary, Union Minister of State for Finance, as well as finance ministers of state and union territories. Senior Ministry of Finance officials, as well as state and UT representatives, attended the meeting.

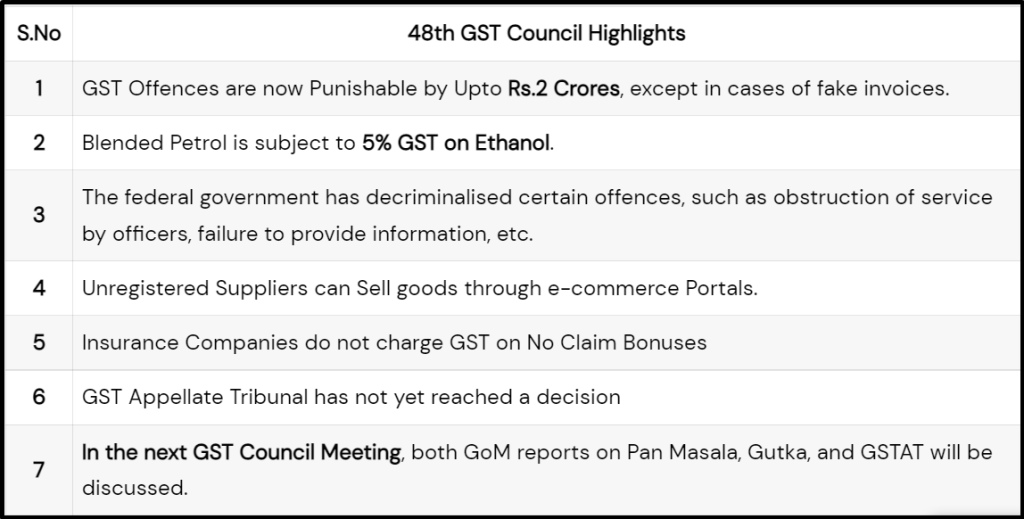

Regarding decriminalizing GST-related offenses, the Council proposed raising the threshold from ₹1 crore to ₹2 crores for launching a prosecution under GST. It would apply to all cases except invoices issued without the provision of goods or services. Additionally, the Council proposed to reduce the compounding amount from 50% to 150% of the tax amount to 25% to 100%. In addition, certain offenses would be decriminalized, including obstruction of an officer in the discharge of their duties, the deliberate falsification of evidence, and failure to provide information, as required.

In addition, the Council proposed to facilitate the use of e-commerce by micro-enterprises. This decision is based on the in-principle approval granted at the previous Council meeting allowing unregistered suppliers and composition taxpayers to make intra-state supplies of goods through an e-commerce operator. As a result of the GST Council’s approval, both the GST Act and the GST Rules have been amended to enable the same. The scheme may be implemented on 1 October 2023.

GST Registration Related:

1. At the time of GST registration now OTP will be sent on mobile no & email id registered with the PAN so that no one can get GST Registration without knowledge of the PAN Holder.

2. GSTN is trying to implement bio-metric-based aadhar authentication & physical verification at the time of registration so that no fake and fraudulent registrations can be taken. Proposal to conduct a pilot in the State of Gujarat.

GST Returns Related:

3. Now the Returns (GSTR 1,3B,9,9C,4, etc ) can only be filed a maximum of 3 years after the Due date. Earlier there is no limit for filing returns, as we know If returns are not filed for 6 months then registration will get suspended but still returns can be filed. But now insertion of restriction in time limit.

4. GSTR-1 FORM will be amended & new tables to be inserted for reporting details of supplies made through ECOs, covered under section 52 and section 9(5).

New GST Forms Related :

5. New form DRC-01B & Rule 88c to be inserted, this will be an intimation form for the Differences in GSTR-1 & GSTR-3B for the tax period if the difference exceeds a specific amount/ percentage limit, so taxpayers have to pay the amount or explain the differences.

If not paid or not explained then the next period GSTR-1 will be restricted & can’t be filed.

this form will be system generated so no involvement of any officer for tax difference payment.

E-invoice Related :

6. Circular will be issued for clarification on the applicability of e-invoices from 1st Jan 2023.

Definition changes Related :

7. Definition of NTOR & OIDAR will be changed to reduce interpretation issues and litigation.

Verification of ITC by department Related :

8. For FY 17-18 & 18-19, a Circular will be issued for clarification about what procedure is followed by department / Officers for verification of ITC in GSTR-3B vis a vis Available in GSTR-2A.

POS Related:

9. For Goods transportation services, a Circulation will be issued for clarifying the Place of Supply & ITC Availability & commission of Section 12(8).

TDS-TCS Deductors Related :

10. facilities will be provided for the cancelation of registration on their request

Demand Related:

11. Circular will be issued for clarification of the re-determination of demand in section 75(2).

For taxpayers Whose IBC Proceedings have finalized Related :

12. Circular to be issued for clarifying the issue of treatment of statutory dues under GST & GST DRC-25 also to be amended.

All Recommendations will be effective from the date when the notification/circulars will be issued.